This week Sudden Debt pays homage to the opening of yet another Star Wars episode. The title comes from the third installment released in 1983, but my version is more recent and less galactic.

========================================

"Greek banks lack earnings visibility."

"There is no story, other than bad loans."

"Their balance sheets are shrinking."

"There are no creditworthy borrowers."

If you are at all familiar with the Greek Depression and its Greek banking saga you have certainly heard one or all of the above. In fact, up until recently I would be the one saying them - but no more. I now strongly believe there is a story and strong earnings visibility for Greek banks.

What's new, you ask, what has changed? To answer that I must first take you back almost a quarter century. In line with Star Wars, let's call it a prequel.

A long time ago in a galaxy far, far away...

In early 1994 the Greek socialist government made a seminal decision: it would do everything necessary to meet the Maastricht criteria for membership to the European Monetary Union and its planned common currency, the euro.

One of its first actions came in May of the same year when it abolished FX and capital controls on the drachma. Speculators immediately attacked, betting on a massive devaluation. However, the Bank of Greece raised short-term interest rates sharply to triple digits and ended the crisis within two months. Speculators who had shorted the drachma withdrew with heavy losses.

What followed was a seven year period of unprecedented prosperity for banks and investors who followed the Convergence Trade: huge profits were made by borrowing foreign exchange at low interest rates (mostly German marks, DEM), exchanging them into Greek drachmas (GRD) and investing at much higher interest rates, either in drachma deposits or high yielding Greek Government bonds (GGBs).

It was a safe bet because the government, acting through the

Bank of Greece, was committed to a slow and predictable devaluation of the DEM/GRD exchange rate (i.e. a sliding peg) which was always less than the cross-currency interest rate differential. In simple terms, investors made, say, 12% in drachmas annually and lost only 8% on the gradual DEM/GRD devaluation. That 4% differential was pure profit. As time went on this differential narrowed with Greek interest rates dropping gradually and eventually converging to other EMU currencies' rates. Thus the name Convergence Trade.

D0zens of local and foreign banks rushed in. Institutions such as JP Morgan, Deutsche Bank, Bank of America, Morgan Stanley, Citibank, UBS, Credit Suisse, HSBC, Merrill Lynch, Goldman Sachs, SocGen, ABN and many, many more were in the drachma market daily. Even the erstwhile Lehman Brothers and Bear Stearns made guest appearances to what was, literally, a "money for nothing" party.. (Well, it wasn't really "nothing": these profits were ultimately paid by Greek taxpayers, the price paid for admission to the eurozone).

Greek banks profited handsomely, too. At the time when retail and corporate banking was sleepy at best, dealing rooms were roaring. Some of them exploded from 5 to 50 employees within just two years, as profits soared and bonuses were lavished on one and all. For several years, over 50% of Greek bank profits came from Convergence trading gains.

As time drew closer to Greece's admission to the eurozone drachma interest rates dropped and the party finally ended in 2001. Dealing room profits dropped sharply and several foreign banks that had set up shop in Athens shut down and moved on.

But what about Greek banks?

At the time, Greek bank shareholders were suffering the effects of a punishing bear market on the Athens Stock Exchange. It was the result of a truly historic bubble that took place in 1997-99, one that saw even mountain goat herders selling their flocks to buy into the craze. Stocks had doubled, and then doubled again and again... it was madness, until the inevitable crash which started in late 1999 and concluded in 2003.

After 2002, however, earnings and share prices recovered strongly as banks focused on retail and corporate lending. Prior to the euro, Greek households and businesses carried very little debt since drachma interest rates were very high. Things changed rapidly after 2002, when a combination of Greece's entry to the eurozone and globally low interest rates post 9/11 events made borrowing cheap and easy. Credit expansion ran at breakneck speed, boosting real estate prices and GDP growth. Shares soared again.

Then the global debt bubble burst in 2007-08.

Greece, facing ever larger budget deficits, and unable to borrow on its own, had to accept bailout loans from the EU and IMF; its bonds suffered deep haircuts. Bad loans inundated bank balance sheets (today NPLs and NPEs amount to approx. 50% of all loans), profits turned into losses and banks were re-capitalized three times, with massive dilution to their original shareholders, who saw their investments collapse 99.5%. Balance sheets contracted by 45% in 2010-17 and the industry consolidated furiously. There are now just four major Greek "systemic" banks, accounting for a whopping 97% of all assets.

OK, enough with the prequel.

What is the sequel? Where are future profits going to come from (visibility), what is the "script" for our Greek Bank Wars?

In my estimation Greek banks are uniquely placed to take advantage of two major opportunities:

========================================

"Greek banks lack earnings visibility."

"There is no story, other than bad loans."

"Their balance sheets are shrinking."

"There are no creditworthy borrowers."

If you are at all familiar with the Greek Depression and its Greek banking saga you have certainly heard one or all of the above. In fact, up until recently I would be the one saying them - but no more. I now strongly believe there is a story and strong earnings visibility for Greek banks.

What's new, you ask, what has changed? To answer that I must first take you back almost a quarter century. In line with Star Wars, let's call it a prequel.

A long time ago in a galaxy far, far away...

In early 1994 the Greek socialist government made a seminal decision: it would do everything necessary to meet the Maastricht criteria for membership to the European Monetary Union and its planned common currency, the euro.

One of its first actions came in May of the same year when it abolished FX and capital controls on the drachma. Speculators immediately attacked, betting on a massive devaluation. However, the Bank of Greece raised short-term interest rates sharply to triple digits and ended the crisis within two months. Speculators who had shorted the drachma withdrew with heavy losses.

What followed was a seven year period of unprecedented prosperity for banks and investors who followed the Convergence Trade: huge profits were made by borrowing foreign exchange at low interest rates (mostly German marks, DEM), exchanging them into Greek drachmas (GRD) and investing at much higher interest rates, either in drachma deposits or high yielding Greek Government bonds (GGBs).

It was a safe bet because the government, acting through the

Bank of Greece, was committed to a slow and predictable devaluation of the DEM/GRD exchange rate (i.e. a sliding peg) which was always less than the cross-currency interest rate differential. In simple terms, investors made, say, 12% in drachmas annually and lost only 8% on the gradual DEM/GRD devaluation. That 4% differential was pure profit. As time went on this differential narrowed with Greek interest rates dropping gradually and eventually converging to other EMU currencies' rates. Thus the name Convergence Trade.

D0zens of local and foreign banks rushed in. Institutions such as JP Morgan, Deutsche Bank, Bank of America, Morgan Stanley, Citibank, UBS, Credit Suisse, HSBC, Merrill Lynch, Goldman Sachs, SocGen, ABN and many, many more were in the drachma market daily. Even the erstwhile Lehman Brothers and Bear Stearns made guest appearances to what was, literally, a "money for nothing" party.. (Well, it wasn't really "nothing": these profits were ultimately paid by Greek taxpayers, the price paid for admission to the eurozone).

Greek banks profited handsomely, too. At the time when retail and corporate banking was sleepy at best, dealing rooms were roaring. Some of them exploded from 5 to 50 employees within just two years, as profits soared and bonuses were lavished on one and all. For several years, over 50% of Greek bank profits came from Convergence trading gains.

As time drew closer to Greece's admission to the eurozone drachma interest rates dropped and the party finally ended in 2001. Dealing room profits dropped sharply and several foreign banks that had set up shop in Athens shut down and moved on.

But what about Greek banks?

At the time, Greek bank shareholders were suffering the effects of a punishing bear market on the Athens Stock Exchange. It was the result of a truly historic bubble that took place in 1997-99, one that saw even mountain goat herders selling their flocks to buy into the craze. Stocks had doubled, and then doubled again and again... it was madness, until the inevitable crash which started in late 1999 and concluded in 2003.

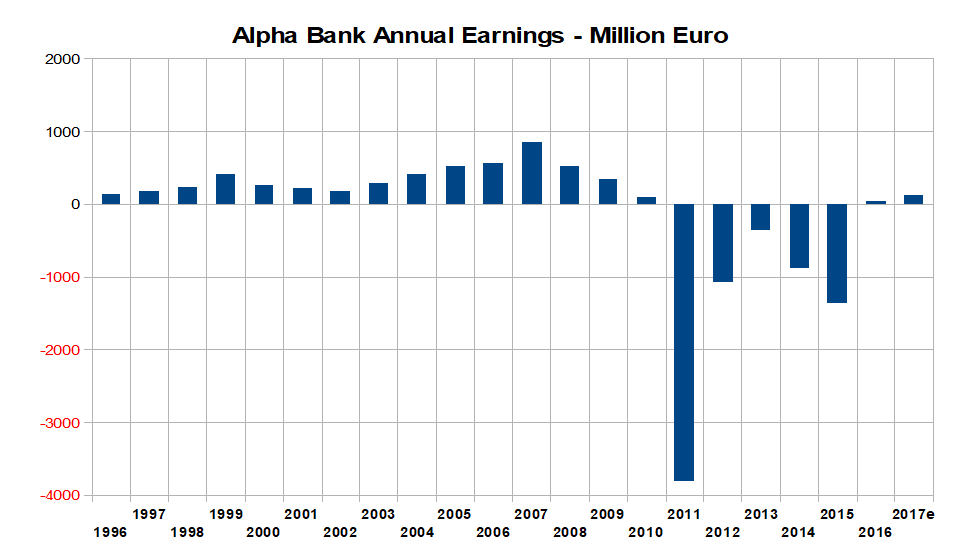

Apart from the effects of the bubble bursting, banks were suffering from the imminent loss of Convergence Trade profits and a lack of future earnings visibility (ring a bell?).

As you can see from the charts for Alpha Bank, after first going ballistic, shares dropped as much as 80% top to bottom between 1999-2003. Earnings fell 58%.

Price of Alpha Bank shares on ASE (split adjusted)

After 2002, however, earnings and share prices recovered strongly as banks focused on retail and corporate lending. Prior to the euro, Greek households and businesses carried very little debt since drachma interest rates were very high. Things changed rapidly after 2002, when a combination of Greece's entry to the eurozone and globally low interest rates post 9/11 events made borrowing cheap and easy. Credit expansion ran at breakneck speed, boosting real estate prices and GDP growth. Shares soared again.

Then the global debt bubble burst in 2007-08.

Greece, facing ever larger budget deficits, and unable to borrow on its own, had to accept bailout loans from the EU and IMF; its bonds suffered deep haircuts. Bad loans inundated bank balance sheets (today NPLs and NPEs amount to approx. 50% of all loans), profits turned into losses and banks were re-capitalized three times, with massive dilution to their original shareholders, who saw their investments collapse 99.5%. Balance sheets contracted by 45% in 2010-17 and the industry consolidated furiously. There are now just four major Greek "systemic" banks, accounting for a whopping 97% of all assets.

OK, enough with the prequel.

What is the sequel? Where are future profits going to come from (visibility), what is the "script" for our Greek Bank Wars?

In my estimation Greek banks are uniquely placed to take advantage of two major opportunities:

- Because of the bailout programs Greek government debt is currently 80% in the form of non-tradeable loans from the official sector - that's 260 billion out of a total 325 billion euro. With a return to more normal conditions, economic growth and increased investor confidence, Greece will seek to slowly at first and then more rapidly, swap official loans with its own bonds. The reason is that the loans impose strict oversight rules that restrict fiscal freedom. Such bonds will initially have attractive spreads over other government bonds and yield far above banks' cost of money, making them ideal profit-generating machines for Greek (and other) banks. Longer term, Greece will seek to replace at least 75% of loans with new GGBs, because that's the level at which oversight is terminated. That's a very nice business for banks, and for a long time, too. Think of it as Convergence Trade II, creating earnings visibility for several years going forward. The convergence has started: 10-year GGBs are now at 3.95% (German Bunds are at 0.30%), the lowest since 2006 and down from nearly 12% in 2016. Two year notes are at 1.95% (German 2-year notes are negative at -0.72%), below even the government's average overall funding cost (approx. 2%). They were at 10% last February.

- Despite the mess in consumer, mortgage and corporate loans, banks are finally and rapidly dealing with their NPLs and NPEs through a combination of loan sales, write-offs and foreclosures/auctions. By the end of 2019 they will have halved their bad loans. Such a bitter medicine leaves a lasting aftertaste to lender and borrower alike. Meaning, Greeks have now gotten a hard lesson in coping with debt and have, at last, acquired a credit ethic. Renewed credit expansion, when it comes, will be based on much firmer ground. And it will come, because banks' assets are now at just 155% of GDP - or even less, when we adjust for the rapid deleveraging from the bad loan reduction. By comparison, Germany is at 261% and Italy at 248%.

Here's the answer: deposits. Yes, deposits - those that fled in a panic during the Greek crisis, going to safe havens abroad, in safe-deposit boxes and under mattresses. Banks in Greece held 281 billion euro in deposits in 2009 (122% of GDP) and a mere 144 billion as of this past October (80% of GDP). But, unlike the US Great Depression, Greek bank customers have not lost a single penny of their deposits. Their money is still intact. Even if we deduct foreign depositors from the 2009 figure above, there is a very, very large pool of money that, given the right conditions, will come rushing back into Greek banks - perhaps as much as 100 billion.

All right... Just like the Star Wars space opera, this has been a larger post than I normally write. Yet, I think the subject is really worth it. Since I don't think readers of Sudden Debt need me to spell out the obvious conclusions (you are much too smart an audience), I will leave you with...

May the Force be with you.

Hell, I have some nagging doubts about this Phoenix--like elevation of Greece. Were it the case that the employment prospects of the younger generations were actually positive, that is wage/salary increases above 3% p/a for at least 7 years in a row, then I would start to pay attention.

ReplyDeleteWage Compression = Revenue Compression -> fiscal trouble. I think. Greece has a shocking problem with refugees from the east. Maybe the ECB will donate GR one mill euro per refugee per annum - so they can be economically assimilated without rendering the whole country esentially ungovernable.

If the ECB was actually mandated by the European Commission to fund each refugee who lands in Europe with a european-style min wage: there would be only a few refugees. Period.

Greek financial institutions may well be recovering their footings, but what about the pulverized Greek consumer? Tinkle Down economics?

Brian, employment and salaries are very lagging indicators, especially coming out of a deep recession. Businesses first meet increased demand with other means (eg overtime) until they are convinced the recovery is solid and then they hire more people.

ReplyDeleteIn tourism, a sector that is showing strong and consistent growth in Greece, employment is is fact strong. The same sector is also showing strong growth in construction, by the way (new hotels, renovations, additions, etc).

Obviously the ECB cannot provide refugee money... not its mandate.

Hell, thanks. The ECB should be mandated to provide financial support for all EU refugees - how else will impoverished these folk be incorporated as useful consumers? Being dependent on charities for your shelter, food and cloths is not funny.

ReplyDeleteGermany was barely able to incorporate its fellows from the DDR. Its taken near enough thirty years - and they still haave makor problems. So how will other EU states manage to absorb economic migrants and refugees? They cannot, because they lack the financial (ie. fiscal) resources to do so. It started badly - its going to end badly.

I note the connection between the improvement of tourism and construction: Barnum and Baily stuff. It may happen that the Greek tourism season can be extended and ramped up - but not by much. And if the majority of employment opps in tourism are min subsistence levels ..... I suspect that there may be a bit of a scrap amongst the Med states for what seems to be a limited number of tourism clients. We will see.

The Greek state needs an awful lot of new tax revenue in order for it to reach the point that it can even begin any sort of an economic recovery. Whether it can engineer a parallel social recovery is another matter entirely.

I suppose its cross-your-fingers time.

If you do not post again before the holiday - my best wishes. We'll be back at this soon enough.

Brian.

Dear Brian,

ReplyDeleteIncorporating refugees is a serious issue, certainly. But, for Greece at least, it's not a major one at this time. Their number is around 60.000, or 0.5% of the total population. Expenses for their care are covered by the EU right now. Some will be granted asylum and perhaps seek to stay permanently, while the rest will hopefully return to their homes when and if things return to normal in the Middle East.

Tourism is Greece's major industry and, with proper development, can continue to grow strongly towards higher added value by becoming more high end. Look at today's post :)

All the best for the Holidays!