I admit it; I am, and have always been, a fan of classic science fiction. Thus, the title of today's post, a direct reference to the

classic novel by Arthur C. Clarke, in which the Golden Age of The Overlords ends and Mankind has to deal with the aftereffects. (Oh,

please... no puns about science fiction and finance, I am the one who coined the phrase "sci-fi finance" (smile)!)

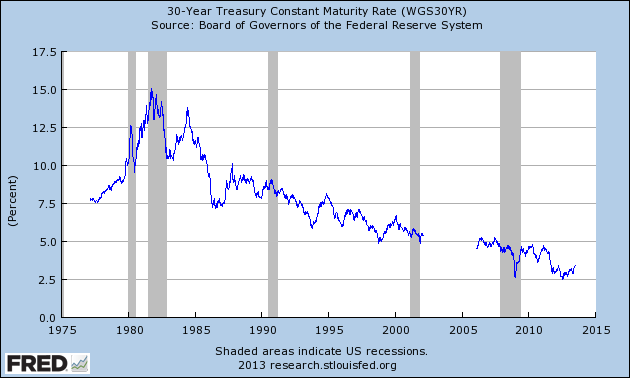

There may be no benign aliens in silver ships circling the skies above, but one could easily be forgiven a tendency to Utopianism when gazing at the following chart. I mean, wtf? (sorry, I have two teen daughters..). Thirty year bonds at 3-ish percent? Have people taken leave of their risk-awareness senses?

Oh no, will chime the pundits.. it's precisely because we think default risk is so high that we accept such piddly returns, at lows not seen since FDR and the Very Great Depression (the one we escaped came close to being GD Part II).

Historical US Treasury Yields

And 10 year Bunds at less than 2%? Mein Gott, deez ist nutz!

10-Year German Bund Yield

Seems that if there is a pig heaven for borrowers, this is it.

Assuming, of course, you are not a PIIGy, in which case you have been occupying a seat in Hell's roller-roaster reserved just for you by Mrs. Merkel, guardian of the EU's not-so-pearly gates. (Yeah, yeah, I know.. everyone is bashing the Germans. Never mind, some of my best friends are Krauts.. er, Germans.)

Ok, what am I driving at? This: If you own AAA/sovereign bonds you are paying WAY too much for credit protection and, conversely, you are accepting WAY too much market (inflation) risk. In simple English, bonds are much too expensive.

No, I'm NOT expecting hyperinflation, I am not a gold bug, a survivalist or any such -ist, but I am an open-minded pragmatist. The global economy will grind to a halt if credit is not made more freely available to the suffering economies of the West, and particularly in Europe which makes up one quarter of the world's GDP.

One way or another, money will have to be shaken out of "safe havens" and into the Real Economy, to finance much needed growth.

To wit, ΙΜΗΟ interest rates are going higher.

{kind=link}