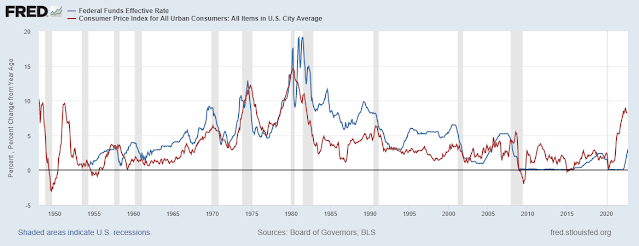

If you read the financial and mainstream press you get the impression that the Fed has embarked on the most aggressive interest rate hikes ever. But even a cursory look at the facts (see chart below) shows it just isn't so, even when we add the75 basis point hike expected today. Moreover, everyone is already talking (hoping) about the Fed tapering its hikes after today.

Fed Funds (Blue line) and Inflation (Red line)

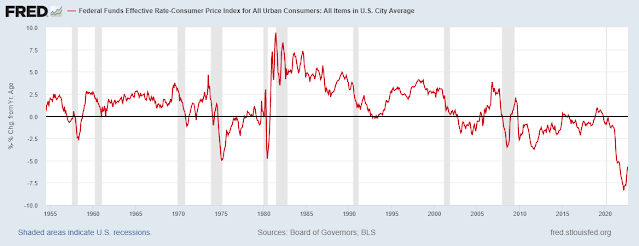

The reason for this rate anxiety, the view that rate hikes are perhaps already excessive, is simple: rates started from zero and hikes look excessive. In fact, they are small given how high inflation is right now. Real Fed Funds (Fed funds minus inflation) are at record negative territory (see below) and are thus having very little, if any, impact on fighting inflation. Instead of being a Rate Superman, the Fed is still a mere MiniMe.

Fed Funds Minus Inflation

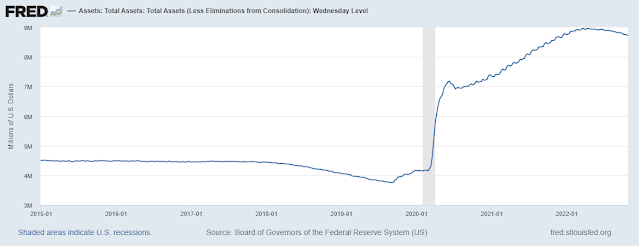

Once again: focusing only on interest rates is wrong, wrong, wrong. The real cause of inflation is excessive liquidity created by the Fed itself via massive QE in a very short period of time, and which is still sitting on its balance sheet undrained (see chart below).

Fed Balance Sheet Assets

If one needs more proof that liquidity is indeed excessive, he/she need look no further than the Fed's own O/N reverse repo, now at a massive $2.2 trillion (see chart below). That's money that banks and other major institutions have no other use for and are electing to park it overnight with the Fed.

Fed O/N Reverse Repo

The Fed is currently draining liquidity at a maximum $90 billion per month. Judging from the size of the reverse repo alone, this pace is too slow to have any meaningful impact on inflation and should be increased immediately, perhaps to a level approaching the initial rate at which liquidity was added during QE, ie around $500-750 billion per month.

It certainly won't reach that level, but $90 billion/month is clearly too little - a monetary policy MiniMe when it comes to inflation fighting.

I can't help but to say it again: its all in the QT - and I really wonder why almost no one is talking about it, at least not widely. I'm becoming suspicious in my old age :)

Steven Pearlstein mentions it in passing towards the end of this piece: https://www.washingtonpost.com/us-policy/2022/11/02/federal-reserve-financial-crisis/

ReplyDeleteBut you're right. It's not being talked about much at all.

Thank you for the article!

Delete