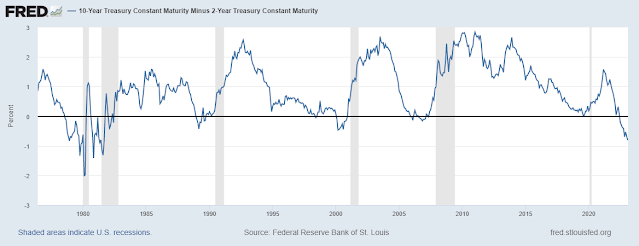

The 10-year minus 2-year Treasury yield spread is considered one of the best recession predictors. When it goes negative, ie when the 2-year note yields more than the 10-year bond, a recession soon follows (chart below, recessions in grey). Will the past repeat?

I think there is something different and unusual about this episode of yield curve inversion.

- For one, it comes after a very prolonged and unprecedented period zero/negative short interest rates. Meaning, short rates were extraordinarily low and had a ways to go higher before they normalized. By comparison, long rates had not fallen as much. Therefore, it is logical for the spread to be more negative than otherwise.

- Secondly, there is a growing feeling that the Fed will be successful in quashing inflation in the next few months, and thus long rates need not be as high as current inflation implies. Therefore, while short term rates are high, long rates are still low ---> spread more negative than otherwise.

Markets are definitely acting along those two concepts above. Are they correct? I have no idea, but if they are not we are going to see a major "disillusionment" drop in all markets.

Putting it another way, the near record negative spread is more an indicator of markets defying the Fed (and common sense) than anything else. It’s an indicator of excessive speculative optimism which may be proven unfounded.

Indeed. Markets are priced to "inflation expectations perfection".

ReplyDelete