Note: Numbers on Debt/GDP below have been calculated using GDP on a Purchasing Power Parity (PPP) basis. Also, I have removed countries such as Lebanon, Suriname, Sudan, etc. from the chart.

__________________________________________________________________________

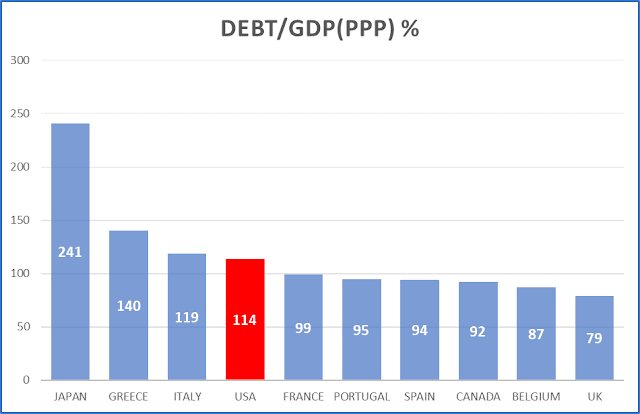

When it comes to Debt/GDP Japan is the undisputed "champion" - but most all of its debt is domestic. Only 6.5% of all debt is owed to foreigners, while the vast majority (52%) is held by the Bank of Japan. This has significant global repercussions, but Japan is not my subject today.

Number two on the rogues list is Greece - no surprise there - but unlike Japan most all of its debt is owed to foreign official sector lenders. The bad news here is that this debt load exists even after the country went bankrupt a decade ago and plunged its economy into a decade long depression. But Greece is also not my subject today.

Numero tre is Italy. A perennial problem child, the only reason Italy can still finance itself at reasonable interest rates is that its Eurozone membership is presumed to preclude a bankruptcy. Let me point out, however, that as recently as 2008 its debt/GDP(PPP) was ca. 70%. But Italy, too, is not my subject today.

My subject today is the USA - not a shock to regular readers of this blog going back as far as 2006. And my main question here is this: how logical, or even safe for the global economy, is it that the issuer of the world's reserve currency is so heavily in debt? Indeed, what does this mean for the US dollar when its issuer is the world's #4 most indebted economy?

Sure, under our current fiat currency regime, where debt is money and money is debt, it is expected that the availability of the global reserve currency can only come from a country that has a commensurately high debt.

But at which point does the debt load finances mostly domestic consumer spending of cheap imports (eg China) and defense spending, instead of productive, high value added activities? At which point does the incessant printing/borrowing become a vicious cycle?

Hint: the crypto boom is stoked to a large extent by those who look at such statistics and rub their hands in glee. I do not share their glee because if we go down that route we are opening a much worse Pandora's Box - no need to enumerate all the nasty stuff that will come out from the Crypto Box.

But... something must be done to contain the US propensity to borrow and spend with abandon as if "tomorrow never comes, la, la, la". Because, unlike in the song, tomorrow always comes.

Let me try to quantify the debt excess, even if roughly: the US accounts for approx. 16% of global GDP(PPP), but its government debt stands at ca. 35% of global government debt. In other words, the US is twice as indebted when measured against its global economic size.

Perhaps the world has no choice but to finance US debt. Where else do they find consumers willing to 'pay' for their goods?

ReplyDeleteThat's a valid point, akin to playing with fire. A merchant can keep financing its customers to generate sales and earnings, but at some point the customers become overextended and renege on their debts. Is the US overextended? I increasingly fear that it is getting there. That's why I included the 16/35% metric in the last paragraph.

ReplyDeleteThis "playing with fire" can go on for some time because social stability is paramount in many countries. They need jobs more than making profits!

DeleteYes, of course - jobs are paramount for social stability. But, in the end, who pays their salaries? In China/Japan/other such countries, it is ultimately their own governments who lend money (buy Treasurys) to Americans to buy their "cheap" imported goods. It's a dead-end way to create jobs, and I'm afraid the end will come a lot sooner than anyone expects.

DeleteI do not like Mr. Trump, but he's right in one (and one only) thing: America needs to bring back its factories, to re-create its once robust working middle class. And that's why his MAGA slogan resonates so strongly in places like Ohio and Pennsylvania...

https://www.ft.com/content/8cd73c44-d47f-4541-a630-c824a0fc1b1d

DeleteThank you Juanita :) Nevertheless, there are today 30% fewer US manufacturing jobs than in 2000 when their number started to collapse .. oh well... please seek the full data in the BLS site here https://data.bls.gov/pdq/SurveyOutputServlet

Deletea different take:

Deletehttps://carnegieendowment.org/chinafinancialmarkets/90358