In yesterday's post I looked at rising prices for US Credit Default Swaps (CDS) as a possible indication for increasing tail risk, ie the possibility of a US default. But then, I got another idea...

Are US CDSs priced correctly to begin with?

First, s bit of background.

The most common way to calculate CDS prices is as bond yield spreads between the "riskier" credit and a "risk free" benchmark. In the eurozone, for example, the benchmark is German bonds - let's look at two countries’ CDSs:

Germany 5 year bond yield: -0.59%

Spain 5 year: -0.34% -----> Spread to Germany = 0.25% or 25 bp

Greece 5 year: +0.07% -----> Spread to Germany = 0.66% or 66 bp

Therefore, we would expect their euro denominated 5 year CDS to be priced at 25 and 66 points respectively. As of Friday, their actual prices were 30 and 75 points. Pretty close, considering that CDSs are almost always more attractive/convenient, and thus more expensive, than putting on a credit spread trade by using the bonds themselves (there are difficulties arising from different coupon payment dates, availability and cost of borrowing bonds to short, etc). So, we can see that Spanish and Greek CDSs are accurately priced in the market.

So, what about the US? How accurately priced are its sovereign CDSs?

The first issue that arises is what benchmark to use in calculating a credit spread. In the US we ASSUME that Treasurys are risk free, so we use them as a benchmark. As of last Friday the 5 year Treasury yield was 0.93%. Therefore, a dollar denominated USA sovereign CDS should be priced at 0.93-0.93% = zero, or nearly. Instead, it is trading at 15 bp. Why?

Well, a CDS is similar to an insurance policy, a contract between the buyer and the seller of the CDS. Therefore, there is counterparty risk involved, mainly that the seller of the CDS won't pay up in case of default. Unlike during 2006-09, the CDS market now widely uses Central Clearing Parties (CCP) to reduce such risk. Organizations like DTCC come between buyers and sellers, aggregating and netting positions, mitigating individual counterparty risk to a significant degree.

Still, there is some residual risk involved and not all trades go through CCPs, so a price of 15 bp above zero is not way out of line. By comparison, the German sovereign CDS is also above zero at 9 points. There are also other, slightly more esoteric reasons why CDSs cannot be at zero, but let’s not go into greater detail. The main question is different: Are US CDSs properly priced on credit risk alone?

What if we were to assume the US was the “riskier” entity and Germany the benchmark “risk free” one? Then, the US CDS should be calculated as:

US 5 Year Treasury - Germany 5 Year Bund = 0.93 - (-0.59) = 1.52% = 152 points

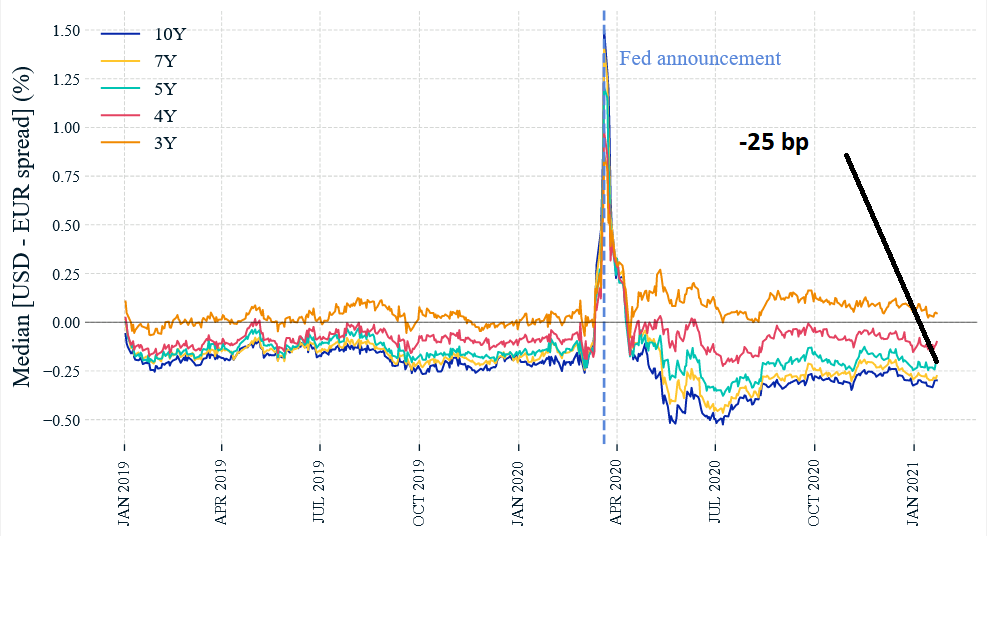

Ah, you say, this is not correct because this is a cross-currency credit spread, euro vs. dollar. You are right, we need to take the FX component into account. I will therefore use the MSCI calculation of USD-EUR cross currency credit spreads - chart below.

|

| USD-EUR 5 Year Credit Spread at -25bp |

Therefore, the theoretical calculation now becomes 152-25 = 127bp for the dollar based US sovereign CDS price. That’s still very far above the market price of 15, by a factor of 8.5x, ie the US CDS is theoretically extremely cheap and greatly underestimates the probability of a US default. Looking at the table of sovereign CDS above, the closest in price to 127 is Mexico at 101, rated BBB with a default probability of 1.70% vs the US AA+ with probability at 0.26%.

Summing it up: if we use the assumption that Germany is a better credit risk than the US (it is) AND we use it to price/benchmark US CDS, then there is a very large price discrepancy, leading to the conclusion that the US sovereign risk is being greatly underestimated by the market.

Why? Because the US cannot default, right? This may ultimately prove to be a very costly assumption, just as in 2006-08 when “house mortgages don’t default, right?

Hi Hell, if the U.S. defaults, the probability of the counter-party paying in meaningful money should be close to zero, making it close to a no win case?

ReplyDeleteIn contrast, there is a chance of making a profit from a German default.

Would this explain some of the price difference?

There are levels of default, one of them being technical. ie delaying the payment of interest and/or principal exactly when due. Some CDS contracts include this case and trigger payment, but not all. Also, there is a recovery clause which limits the amount paid on CDS.

ReplyDeleteAnyway, the point is not so much what happens AFTER default as the pricing of US credit risk right now. I believe it is way underpriced precisely because it is "unthinkable".

In addition, there are lots of other issues that arise. CDSs are not as popular as they once were back in 2006-08 when they came crashing down, the volume outstanding has come down sharply. But there are other interest rate derivatives out there... i'll write about them in tomorrow's post.. :) stay tuned.

great, will look forward to it =)

Deletebtw, following up my old chain of thought

ReplyDeletehttps://www.youtube.com/watch?v=vCad77_c-LU

maybe, when we take away natural selection, we have genetic and social meltdown; that is harmful genes, habits and ideas are not selected away, instead they build up in soceity.

Here's a very recent relevant editorial in the NYT by none other than Haank Paulson ex Treasury Secretary and ex CEO of Goldman Sachs...

Deletehttps://www.nytimes.com/2021/09/30/opinion/animal-extinction.html