HAPPY NEW YEAR!!

The Fed runs an overnight deposit facility for banks and money market funds known as the O/N Reverse Repo (ONRR). Technically it is a sale and buyback operation (repo = repurchase) of Treasury securities on the Fed's portfolio. Practically, it is a deposit backed by Treasuries. The Fed currently pays interest at a very substantial 4.30% in order to keep its monetary policy tight, ie maintain short term rates in line with its target of around 4.25-4.50%.

The amount deposited just reached yet another all time high of $2.55 trillion - yes, that trillion with a T. Window-dressing is always a factor at year end, but it is still an absolutely enormous amount of money being parked, ultimately at the expense of the American taxpayer.

Doing a quick calculation, at this level it costs the Fed $110 billion annualized in interest. Some observations:

- The $110 billion is, of course, new money that enters the system, ie it is a form of QE. Since the Fed is removing approx. $95 billion/month in its QT operations, the ONRR makes QT considerably less effective on the whole (12x95-110 = $1.03 trillion vs $1.14 trillion of liquidity withdrawn).

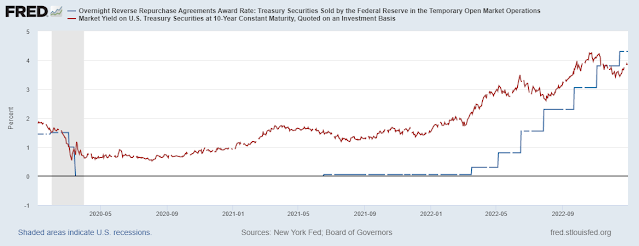

- The interest rate paid at 4.30% is now higher, and significantly so, than the average earned by the Fed on its Treasury portfolio. In other words, the Fed is running the ONRR at a net loss. The chart below shows the ONRR rate (blue) and the current yield on 10-year Treasuries (red). And keep in mind that the Fed is likely earning substantially less on its overall portfolio than the current yield of 10 year bonds. If I had to guess, I would say the Fed has a negative carry of around 100 bp (1%) on its ONRR, or around $25.5 billion per year (again, current levels annualized). *** Addendum: I'm being too conservative here: the likely negative carry is DOUBLE that. I just looked at the Fed's 3Q22 income statement and I calculate a current yield on its portfolio of only approx. 2%. This means the Fed is borrowing $2.55 trillion at 4.30% and lending it out to the Treasury/mortgage originators at 2%... do the math: 2.55x(4.30-2.00) = $58.6 billion negative carry.

Digging a little deeper into the Fed's 3Q22 financial statement we see that their Net Interest Income (NII) (interest received minus interest paid) for the first 9 months of 2022 came to $83 billion and for the 3Q alone to $13.8 billion - meaning that while the first two months were running at $34.6 billion each, the third quarter NII collapsed by -60%. And it's - essentially - all because of the enormous drain of the ONRR.

- Fight inflation by reducing money supply more aggressively

- Stop increasing money supply via paying interest on the ONRR

- Stop losing money on the negative carry.

No comments:

Post a Comment